Abstract

Previous white papers covered the basics of datacenter power consumption and the frantic pace of growth and general challenges facing utilities responsible for supplying these mass consumers. Northern Virginia is the largest datacenter market in the world, containing over one eighth of the world’s operational capacity. This concentration of demand leads to significant challenges, leading the state government to request the Joint Legislative Audit and Review Commission (JLARC) Report 598, titled “Data Centers in Virginia 2024”. The report is wide-ranging in policy recommendations and analysis; here we are going to focus on the discussion of grid-related challenges and recommendations. While the data and recommendations in the report are written for Virginia, the general principles apply to any region supporting datacenters.

Virginia Background

Virginia’s “Datacenter Alley”, a handful of suburban counties outside Washington, D.C., holds the world’s most critical concentration of hyperscale datacenter capacity, driven by an inherent technical advantage in fiber network backbones. Datacenter infrastructure is being deployed at a pace that is rapidly outrunning the ability of the state’s utility infrastructure to support it reliably. This conflict is intensified by the technical evolution of the modern datacenter, which has shifted from being a large, predictable load to an ultra-dense, localized power consumer. These facilities now draw power at a rate 10 to 50 times greater per square foot than standard industrial buildings, resulting in localized power spikes and extreme thermal management needs. The direct consequence is a critical, near-term strain on the entire electrical grid ecosystem. Forecasts indicate that the state’s unconstrained power demand is set to double in the next decade, with this growth driven almost entirely by the datacenter sector. This explosive, concentrated demand necessitates monumental infrastructure expansion across three energy dimensions: new generation capacity, significant transmission upgrades, and the management of massive thermal and environmental footprints (cooling water, noise, and backup power emissions).

Current Consumption and Forecasted Demand

The shift from a manageable industrial load to a grid-altering phenomenon is best quantified by analyzing the current consumption footprint and the official load forecasts provided to Virginia’s utility planners.

As of the JLARC Report 598 (2024) analysis, Northern Virginia’s datacenters collectively draw an instantaneous peak load of approximately 4,100 to 4,500 Megawatts (MW). To put this figure into context, one large hyperscale datacenter can consume over 100 MW of power, a load greater than most traditional industrial complexes. The rapid accumulation of these facilities has resulted in datacenters consuming approximately 26% of Virginia’s total electricity supply, making them the largest and most rapidly expanding electricity load sector in the state. Historically, the state’s overall energy demand remained flat or declined due to efficiency improvements, but datacenter growth has sharply reversed this trend, leading to significant net demand increases.

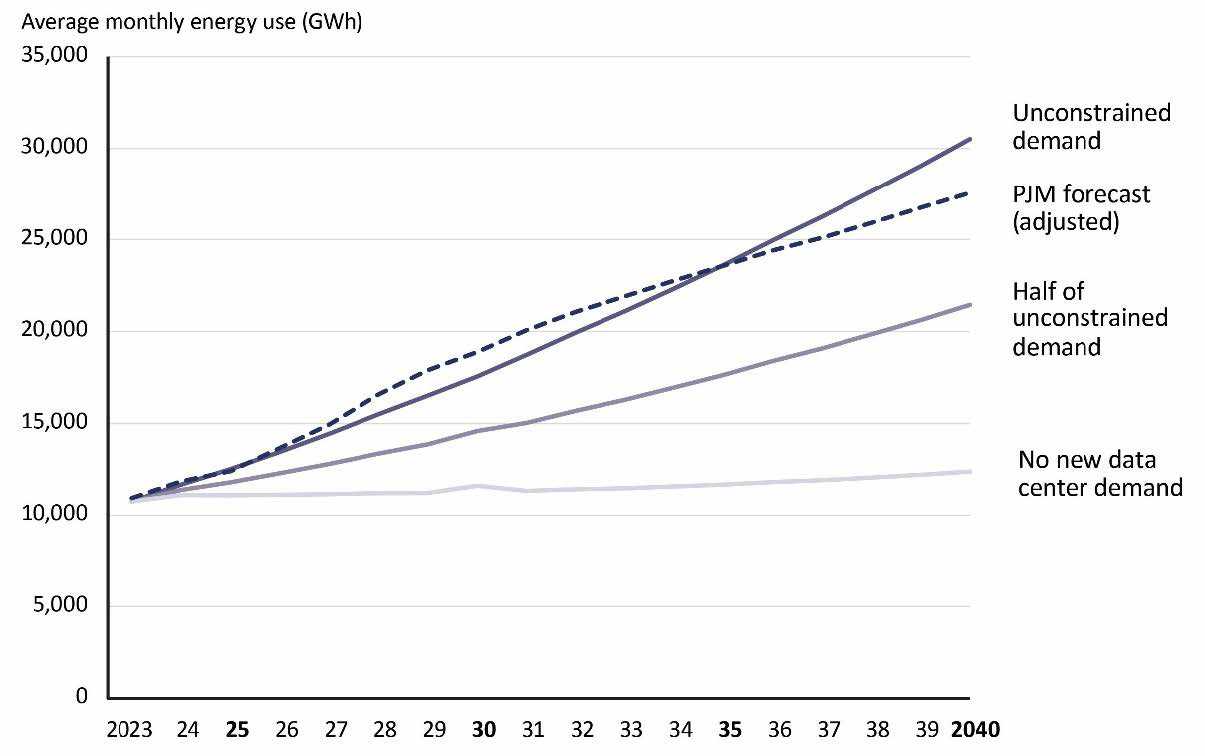

The most pressing technical concern stems from the forecast for unconstrained demand, the amount of power required if all currently planned and projected datacenter projects are built and connected. The forecast commissioned by JLARC indicates that Virginia’s total electricity consumption could nearly triple by 2040, with datacenters responsible for virtually all of that growth. More immediately, the unconstrained demand for power is projected to double within the next decade.

This projected load growth requires a comparison to Virginia’s existing generation assets to illustrate the infrastructure gap: a planned datacenter campus is now expected to consume well over 1,000 MW, a single location requiring more instantaneous power than the 950 MW capacity of North Anna, the state’s largest nuclear reactor. The scale of this future demand requires the state to build an unprecedented volume of new generation and transmission infrastructure simply to keep pace.

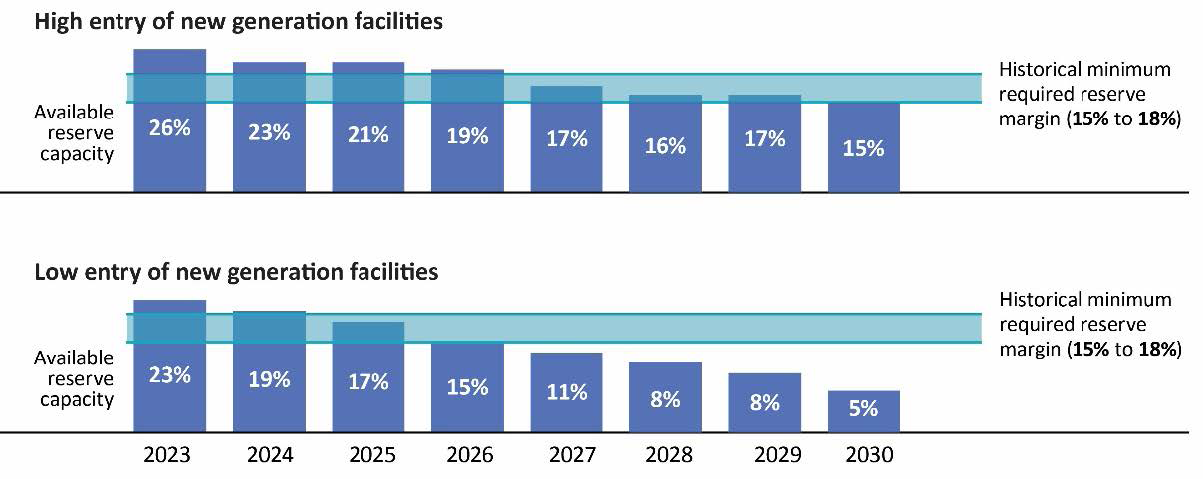

The coordination of this monumental infrastructure expansion falls under the jurisdiction of the PJM Interconnection, the regional transmission organization (RTO) that manages the wholesale electricity grid for Virginia and 12 other states. PJM’s core function is to ensure regional grid reliability by requiring utilities to secure sufficient generation capacity plus a reserve margin.

The technical risk is centered on the speed of the interconnection queue. Datacenters require reliable, firm service, meaning power must be secured for them years in advance. The volatile and rapid load growth from datacenters, however, has overwhelmed PJM’s ability to process new generation and transmission projects fast enough. This uncertainty creates two major reliability issues: capacity shortfall and increased capacity costs. Utilities may not be able to build the necessary power plants and lines in time to serve the massive new load, potentially leading to localized reliability violations. The high demand for firm capacity is driving up costs in PJM’s capacity auctions, an expense ultimately passed on to all ratepayers, further destabilizing the economics of the grid.

PJM is now being forced to consider drastic measures, such as mandating Interruptible Service for large new loads, where datacenters could face power curtailments during grid emergencies until they bring their own supplemental generation or storage online. This indicates a systemic recognition that the traditional grid planning process can no longer accommodate the unconstrained trajectory of datacenter growth.

Challenges: Generation and Transmission

The immense forecasted demand creates an infrastructure gap that cannot be addressed by typical incremental utility planning, forcing state policymakers and utility providers to evaluate drastic, large-scale generation build-out scenarios. The independent analysis commissioned by JLARC provides two primary scenarios to illustrate the difficulty of meeting this rapid load growth.

The first scenario explores the requirements necessary to meet Unconstrained Demand (Scenario 1), which would necessitate building enough new solar facilities at twice the annual rate they were added in 2024, alongside a volume of new wind generation that would exceed the potential capabilities of all offshore wind sites currently secured for future development. Even with this unprecedented pace of renewable deployment, this scenario would still require the construction of large-scale, new natural gas plants and would rely on energy from yet unproven nuclear technologies. Building enough infrastructure to meet even half of Unconstrained Demand (Scenario 2) presents equally difficult challenges. If Virginia Clean Economy Act (VCEA) requirements were ignored, this scenario would demand the construction of a large, 1,500 MW natural gas plant approximately every two years for 15 consecutive years, a rate equal to the busiest period of gas plant construction the state has seen in the last decade. If VCEA requirements were maintained, the greatest challenges would shift to deploying several times the current amount of battery storage, alongside significant new wind generation and natural gas peaker plants. Both scenarios underscore that, regardless of the desired energy mix, the sheer volume of new capacity required cannot be secured without a radical acceleration of permitting and construction timelines.

Beyond securing new generation, the datacenter boom creates an intense and localized transmission crisis, particularly around the Interzonal transfer limits within the PJM grid. Building transmission is a highly time-consuming and capital-intensive endeavor, often taking a decade or more from conception to operation. The high concentration of datacenters in Northern Virginia means power must be physically delivered into a specific, constrained zone. The rapid and unpredictable speed of datacenter deployment has consistently overwhelmed the transmission study and construction process, creating a bottleneck that severely limits the ability of new generation to flow into the demand centers. This issue is compounded by the fact that the datacenter load is often being sited far ahead of the necessary transmission lines being built, leading to massive, unexpected system upgrade costs that must eventually be absorbed by all customers across the utility’s service territory.

Grid Integration Constraints

The JLARC report also highlights a number of non-electrical challenges posed by the rapid expansion of datacenters. The high-density power draw necessitates aggressive thermal management, primarily through evaporative cooling. This creates a significant make-up water load on utility-grade water infrastructure. In 2023, Virginia’s datacenters consumed over 2.1 billion gallons of water. This operational demand requires precise forecasting of water utility capacity and increasing effluent management needs. The consumption is directly tied to the Power Usage Effectiveness (PUE) of the cooling systems and introduces a critical factor for water utility system reliability, particularly in drought-prone areas where competition with potable supply is acute.

The expansive physical footprint, exceeding 390 million square-feet proposed or under construction, creates significant industrial siting constraints and land-use conflicts. From an engineering perspective, the proximity of these large industrial facilities to sensitive loads (residential areas) creates challenges in managing acoustic signatures. The constant operation of cooling towers and HVAC systems, along with the required weekly or monthly testing of the massive on-site backup diesel generator fleet, generates predictable and unpredictable high-decibel noise events. Compliance with increasingly strict local noise ordinances (e.g., limiting nighttime noise in residential areas) requires utilities to engage with advanced acoustic mitigation strategies for substation equipment and transmission infrastructure near these sites.

The non-routine capital expenditure required to service the unconstrained load introduces substantial ratepayer risk and challenges for load-cost allocation. Since the required generation and transmission build-out would not be necessary in the absence of datacenter demand, the fixed costs of these capital projects must be specifically and fairly recovered. The risk is compounded by the threat of stranded assets, infrastructure built years in advance based on aggressive forecasts that may not fully materialize due to market shifts or project delays. Utilities and regulatory commissions must design rate structures and tariffs that appropriately allocate the financial risk of these massive capital outlays to the benefiting customers, thus protecting general service ratepayers from bearing the cost of over-forecasting or under-utilization.

Policy Recommendations

The JLARC report proposes some recommendations to mitigate the systemic risks posed by unconstrained datacenter growth. These recommendations are still proposals, but relevant because they represent government perspective in one of the world’s largest datacenter markets.

Recommendation 1: Load certification must be standardized and mandatory prior to the commencement of deep interconnection studies. Utilities should be empowered to require binding, certified forecasts that guarantee load over a 5-10 year horizon, with financial penalties for major deviations. New datacenter projects should be required to demonstrate and secure firm capacity sufficient to meet their entire operational load before receiving final permitting. This policy compels the datacenter industry to secure or contribute to the creation of necessary generation capacity, rather than relying solely on the general rate base to backstop their immediate demands.

Recommendation 2: The speed of datacenter deployment requires an acceleration of the interconnection queue, which necessitates PJM reform. Utilities should explore proactive Interzonal Transmission Upgrades through accelerated permitting processes, prioritizing infrastructure that unlocks capacity in heavily constrained zones. This includes streamlining the siting and approval of large substations and major transmission lines necessary to distribute power from external, less congested generation sources into Datacenter Alley. Furthermore, regulatory support should be provided for pilot programs utilizing advanced transmission technologies (e.g., High-Voltage Direct Current systems) to increase throughput in constrained corridors.

Recommendation 3: To reduce the reliance on peak grid capacity, new interconnection agreements for large datacenter loads must include mandatory terms for Interruptible Service and the integration of on-site storage/generation. The creation of a favorable regulatory framework for Behind-the-Meter (BTM) Generation Assets is essential. This encourages datacenters to incorporate large-scale battery storage or fuel cells that can operate during grid emergencies or high-cost peak events, effectively reducing their demand on the PJM capacity market. This mechanism serves as a hedge against capacity shortfalls and directly improves regional grid resilience.

Recommendation 4: To address the risk of cost externalization, utility commissions must develop new rate structures that specifically allocate the incremental cost of the required generation and transmission build-out to the datacenter sector. This requires the development of Data Center-Specific Tariffs (DCSTs) designed to recover the full, long-term capital costs associated with new infrastructure dedicated to servicing this load. Furthermore, mechanisms must be established to manage the risk of stranded assets, such as mandatory long-term service contracts or financial assurances from developers, ensuring that general ratepayers are not left bearing the cost of infrastructure for canceled or downsized projects.

Conclusion

JLARC Report 598 transforms datacenters from privileged customers to regulated grid participants. Virginia’s experience—1,500 MW synchronized trips, weak grid pockets, and stranded capacity—previews national challenges as AI drives exponential load growth. The technical requirements emerging from Virginia will likely template national standards: continuous 100th order harmonic monitoring, inverter zone protection coordination, and battery storage replacing diesel generators.

For power quality engineers, Virginia demonstrates that traditional tools and standards prove inadequate when customers rival generator scales. The convergence of millisecond load variations, synchronized protection settings, and weak grid conditions demands new analytical approaches. As JLARC concludes, treating symptoms through grid investment without addressing root causes—uncoordinated development, socialized costs, and absent grid-support obligations—ensures crisis continuation. Virginia’s regulatory framework, however imperfect, represents a comprehensive attempt to balance digital infrastructure growth with grid reliability.